This accounting problem is solved step by step below, with detailed explanations to help you understand the method and arrive at the correct answer.

ScanSolve AI Answer

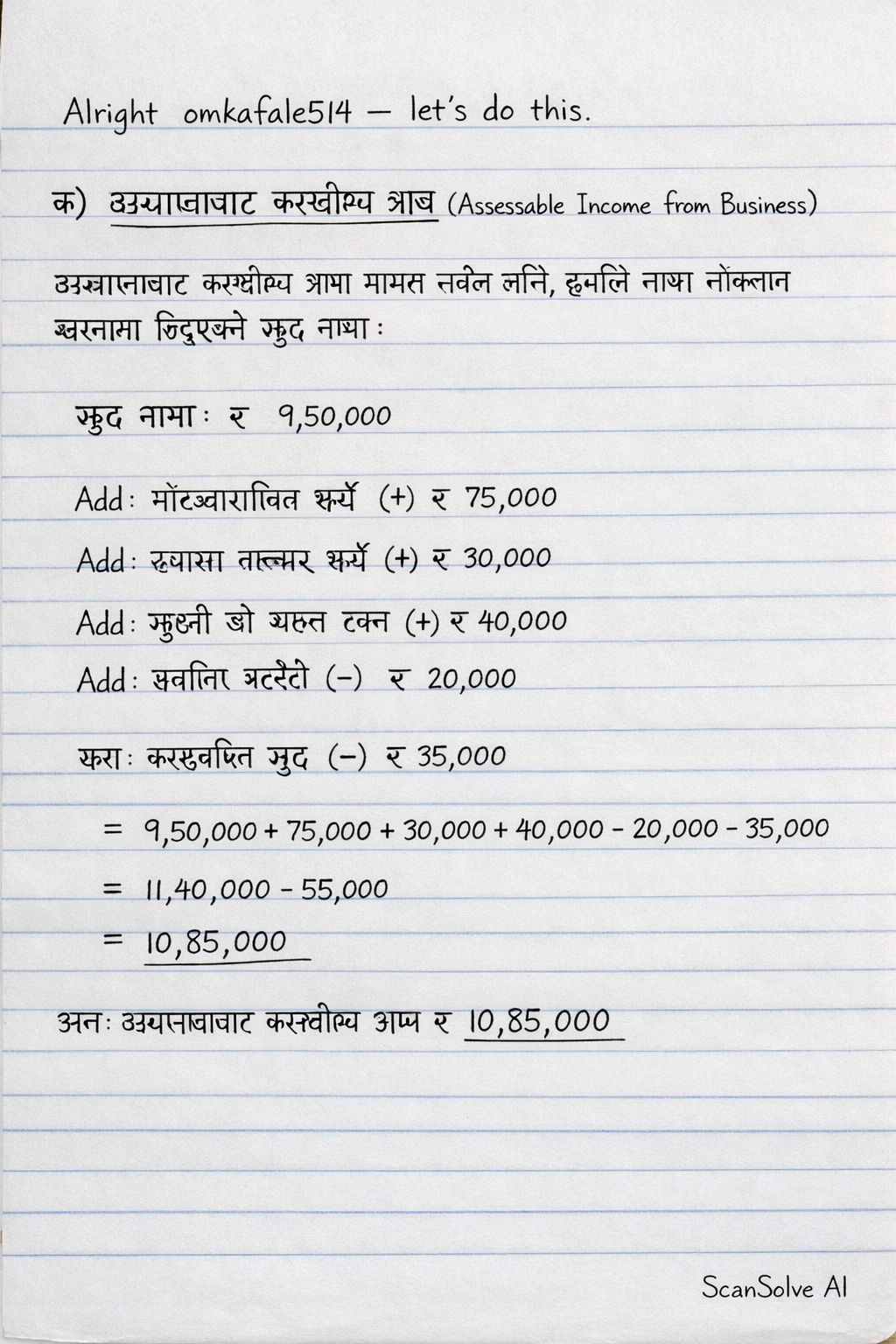

क) व्यवसायबाट करयोग्य आय (Assessable Income from Business) व्यवसायबाट करयोग्य आय गणना गर्नका लागि, हामीले नाफा नोक्सान खातामा दिइएको खुद नाफालाई विभिन्न समायोजनहरू गर्नुपर्छ। खुद नाफा (Net Profit as per P/L A/c) &= Rs. 14,94,000 \\ \\ जोड्नुहोस् (Add): & \\ १. प्रारम्भिक स्टकको अधिक मूल्याङ्कन (Overvaluation of Opening Stock) &= Rs. 1,80,000 - ((1,80,000)/(1.20)) = Rs. 30,000 \\ २. अस्वीकृत ह्रासकट्टी (Disallowed Depreciation) &= Rs. 20,000 - ((20,000)/(1.10)) = Rs. 1,818.18 \\ ३. ट्रेडमार्क खरिद (पुँजीगत खर्च) (Trademark purchase - capital expenditure) &= Rs. 1,20,000 \\ ४. दान (व्यवसाय खर्च होइन) (Donation - not business expense) &= Rs. 90,000 \\ ५. व्यक्तिगत स्वास्थ्य खर्च (Self-medical expenses - personal) &= Rs. 20,000 \\ ६. आयकर अधिकारी विरुद्धको मुद्दाको कानूनी खर्च (Legal expenses for case against ITO - disallowed) &= Rs. 20,000 \\ ७. प्यान नभएका कर्मचारीलाई तलब (Salaries to staff without PAN - disallowed) &= Rs. 20,000 \\ ८. व्यवसायिक सम्पत्ति बिक्रीमा नोक्सान (पुँजीगत नोक्सान) (Loss on sale of business assets - capital loss) &= Rs. 36,000 \\ जम्मा जोड्नुपर्ने रकम &= Rs. 3,37,818.18 \\ \\ घटाउनुहोस् (Less): & \\ १. अन्तिम स्टकको अधिक मूल्याङ्कन (Overvaluation of Closing Stock) &= Rs. 1,95,000 - ((1,95,000)/(1.20)) = Rs. 32,500 \\ २. ट्रेडमार्कको स्वीकृत परिशोधन (Allowable Amortization of Trademark) &= Rs. (1,20,000)/(70 महिना) × 12 महिना = Rs. 20,571.43 \\ ३. आयकर फिर्ता (व्यवसाय आय होइन) (Income Tax Refund - non-business portion) &= Rs. 2,00,000 - 10,000 = Rs. 1,90,000 \\ ४. लगानीमा ब्याज (व्यवसाय आय होइन) (Interest on investment - non-business) &= Rs. 40,000 \\ ५. आवासीय कम्पनीबाट लाभांश (व्यवसाय आय होइन) (Dividend from resident co. - non-business) &= Rs. 2,20,000 \\ ६. गैर-व्यवसायिक सम्पत्ति बिक्रीमा लाभ (व्यवसाय आय होइन) (Gain on sales of non-business assets - non-business) &= Rs. 1,70,000 \\ ७. कृषि आय (कर छुट) (Agriculture incomes - exempt) &= Rs. 1,40,000 \\ ८. चिट्ठाबाट प्राप्त आय (खुद) (व्यवसाय आय होइन) (Lottery received (net) - non-business) &= Rs. 70,000 \\ जम्मा घटाउनुपर्ने रकम &= Rs. 8,63,071.43 \\ \\ व्यवसायबाट करयोग्य आय (Assessable Income from Business) &= Rs. 14,94,000 + 3,37,818.18 - 8,63,071.43 \\ &= Rs. 9,68,746.75 ख) लगानीबाट करयोग्य आय (Assessable Income from Investment) लगानीमा ब्याज (Interest on investment) &= Rs. 40,000 \\ आवासीय कम्पनीबाट लाभांश (Dividend from resident co.) &= Rs. 2,20,000 \\ गैर-व्यवसायिक सम्पत्ति बिक्रीमा लाभ (Gain on sales of non-business assets) &= Rs. 1,70,000 \\ चिट्ठाबाट प्राप्त आय (खुद) (Lottery received (net)) &= Rs. 70,000 \\ लगानीबाट करयोग्य आय (Assessable Income from Investment) &= Rs. 40,000 + 2,20,000 + 1,70,000 + 70,000 \\ &= Rs. 5,00,000 ग) कुल करयोग्य आयको विवरण (Statement of Total Taxable Income) व्यवसायबाट करयोग्य आय (Assessable Income from Business) &= Rs. 9,68,746.75 \\ लगानीबाट करयोग्य आय (Assessable Income from Investment) &= Rs. 5,00,000 \\ कुल करयोग्य आय (Total Assessable Income) &= Rs. 9,68,746.75 + 5,00,000 \\ &= Rs. 14,68,746.75 \\ \\ घटाउनुहोस्: अघिल्लो वर्षको नोक्सान (Less: Brought forward loss) &= Rs. 1,50,000 \\ कुल करयोग्य आय (Total Taxable Income) &= Rs. 14,68,746.75 - 1,50,000 \\ &= Rs. 13,18,746.75 घ) कर दायित्व (Tax Liabilities) श्री जोशी एक व्यक्ति हुन् र उनको व्यवसाय विशेष उद्योग अन्तर्गत पर्दछ। त्यसैले, करका दरहरूमा विशेष छुट लागू हुनेछ। नेपालमा व्यक्तिगत आयकरको सामान्य स्ल्याब दरहरू (विशेष उद्योगका लागि परिमार्जित दरहरू सहित): पहिलो Rs. 4,00,000 मा 1\% &= Rs. 4,000 \\ अर्को Rs. 1,00,000 मा 10\% &= Rs. 10,000 \\ अर्को Rs. 2,00,000 मा 20\% &= Rs. 40,000 \\ जम्मा करयोग्य आय (Total Taxable Income) &= Rs. 13,18,746.75 \\ माथिका स्ल्याबमा कर लगाइएको आय &= Rs. 4,00,000 + 1,00,000 + 2,00,000 = Rs. 7,00,000 \\ बाँकी करयोग्य आय (Remaining Taxable Income) &= Rs. 13,18,746.75 - 7,00,000 = Rs. 6,18,746.75 \\ \\ बाँकी Rs. 6,18,746.75 मा 20\% (सामान्य 30\% को सट्टा) &= Rs. 1,23,749.35 \\ \\ कुल कर दायित्व (Total Tax Liability) &= Rs. 4,000 + 10,000 + 40,000 + 1,23,749.35 \\ &= Rs. 1,77,749.35 अर्को प्रश्न पठाउनुहोस् 📸