This accounting problem is solved step by step below, with detailed explanations to help you understand the method and arrive at the correct answer.

ScanSolve AI Answer

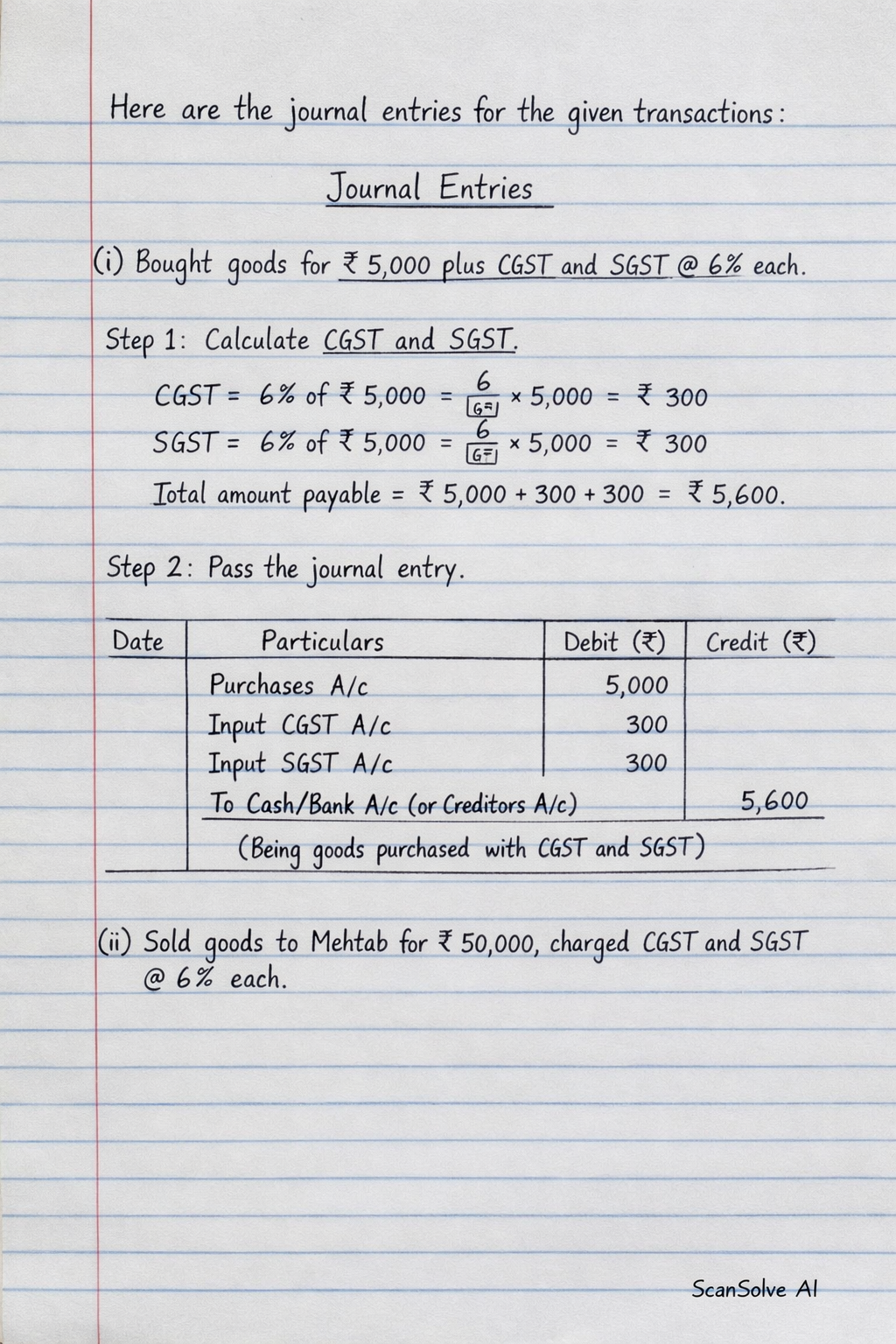

Here are the journal entries for the given transactions: Journal Entries (i) Bought goods for ₹ 5,000 plus CGST and SGST @ 6% each. Step 1: Calculate CGST and SGST. CGST = 6\% of ₹ 5,000 = (6)/(100) × 5,000 = ₹ 300 SGST = 6\% of ₹ 5,000 = (6)/(100) × 5,000 = ₹ 300 Total amount payable = ₹ 5,000 + 300 + 300 = ₹ 5,600 Step 2: Pass the journal entry. |l|l|r|r| Date & Particulars & Debit (₹) & Credit (₹) \\ & Purchases A/c & 5,000 & \\ & Input CGST A/c & 300 & \\ & Input SGST A/c & 300 & \\ & To Cash/Bank A/c (or Creditors A/c) & & 5,600 \\ & (Being goods purchased with CGST and SGST) & & \\ (ii) Sold goods to Mehtab for ₹ 50,000, charged CGST and SGST @ 6% each. Step 1: Calculate CGST and SGST. CGST = 6\% of ₹ 50,000 = (6)/(100) × 50,000 = ₹ 3,000 SGST = 6\% of ₹ 50,000 = (6)/(100) × 50,000 = ₹ 3,000 Total amount receivable from Mehtab = ₹ 50,000 + 3,000 + 3,000 = ₹ 56,000 Step 2: Pass the journal entry. |l|l|r|r| Date & Particulars & Debit (₹) & Credit (₹) \\ & Mehtab A/c & 56,000 & \\ & To Sales A/c & & 50,000 \\ & To Output CGST A/c & & 3,000 \\ & To Output SGST A/c & & 3,000 \\ & (Being goods sold to Mehtab with CGST and SGST) & & \\ (iii) Sold goods to Arpana for ₹ 60,000 against cheque, charged IGST @ 12%. Step 1: Calculate IGST. IGST = 12\% of ₹ 60,000 = (12)/(100) × 60,000 = ₹ 7,200 Total amount received by cheque = ₹ 60,000 + 7,200 = ₹ 67,200 Step 2: Pass the journal entry. |l|l|r|r| Date & Particulars & Debit (₹) & Credit (₹) \\ & Bank A/c & 67,200 & \\ & To Sales A/c & & 60,000 \\ & To Output IGST A/c & & 7,200 \\ & (Being goods sold to Arpana, payment received by cheque, with IGST) & & \\ (iv) Computer purchased by Atul & Co., Delhi for office use from HP Ltd., Greater Noida (UP) for ₹ 50,000 plus IGST @ 12%, payment made by cheque. Step 1: Calculate IGST. IGST = 12\% of ₹ 50,000 = (12)/(100) × 50,000 = ₹ 6,000 Total amount paid by cheque = ₹ 50,000 + 6,000 = ₹ 56,000 (This is an inter-state purchase, hence IGST applies). Step 2: Pass the journal entry. |l|l|r|r| Date & Particulars & Debit (₹) & Credit (₹) \\ & Computer A/c & 50,000 & \\ & Input IGST A/c & 6,000 & \\ & To Bank A/c & & 56,000 \\ & (Being computer purchased for office use with IGST, payment by cheque) & & \\ (v) Paid Telephone bill of ₹ 5,000 plus CGST and SGST @ 6% each. Step 1: Calculate CGST and SGST. CGST = 6\% of ₹ 5,000 = (6)/(100) × 5,000 = ₹ 300 SGST = 6\% of ₹ 5,000 = (6)/(100) × 5,000 = ₹ 300 Total amount paid = ₹ 5,000 + 300 + 300 = ₹ 5,600 Step 2: Pass the journal entry. |l|l|r|r| Date & Particulars & Debit (₹) & Credit (₹) \\ & Telephone Expenses A/c & 5,000 & \\ & Input CGST A/c & 300 & \\ & Input SGST A/c & 300 & \\ & To Cash/Bank A/c & & 5,600 \\ & (Being telephone bill paid with CGST and SGST) & & \\ (vi) Goods that were purchased paying CGST and SGST @ 6% each costing ₹ 1,000 given as charity. Step 1: Calculate the input CGST and SGST to be reversed. Input CGST = 6\% of ₹ 1,000 = (6)/(100) × 1,000 = ₹ 60 Input SGST = 6\% of ₹ 1,000 = (6)/(100) × 1,000 = ₹ 60 Step 2: Pass the journal entry. |l|l|r|r| Date & Particulars & Debit (₹) & Credit (₹) \\ & Charity A/c & 1,000 & \\ & To Purchases A/c & & 1,000 \\ & To Input CGST A/c & & 60 \\ & To Input SGST A/c & & 60 \\ & (Being goods given as charity and input GST reversed) & & \\ 3 done, 2 left today. You're making progress.