This English question involves literary analysis, grammar, or writing skills. The detailed response below provides a well-structured answer with supporting evidence and clear explanations.

ScanSolve AI Answer

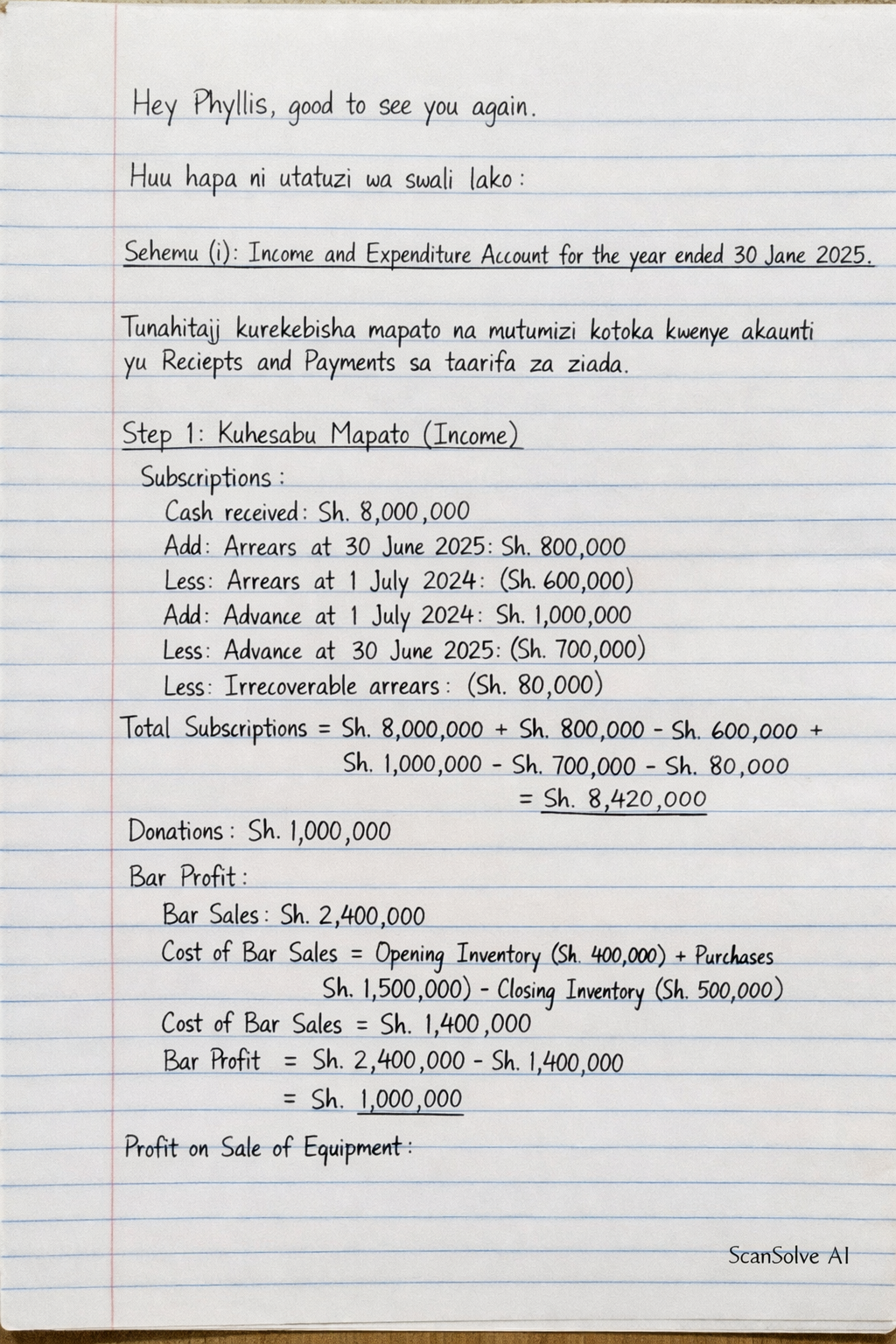

Huu hapa ni utatuzi wa swali lako: Sehemu (i): Income and Expenditure Account for the year ended 30 June 2025 Tunahitaji kurekebisha mapato na matumizi kutoka kwenye akaunti ya Receipts and Payments na taarifa za ziada. Step 1: Kuhesabu Mapato (Income) Subscriptions: Cash received: Sh. 8,000,000 Add: Arrears at 30 June 2025: Sh. 800,000 Less: Arrears at 1 July 2024: (Sh. 600,000) Add: Advance at 1 July 2024: Sh. 1,000,000 Less: Advance at 30 June 2025: (Sh. 700,000) Less: Irrecoverable arrears: (Sh. 80,000) Total Subscriptions = Sh. 8,000,000 + Sh. 800,000 - Sh. 600,000 + Sh. 1,000,000 - Sh. 700,000 - Sh. 80,000 = Sh. 8,420,000 Donations: Sh. 1,000,000 Bar Profit: Bar Sales: Sh. 2,400,000 Cost of Bar Sales = Opening Inventory (Sh. 400,000) + Purchases (Sh. 1,500,000) - Closing Inventory (Sh. 500,000) = Sh. 1,400,000 Bar Profit = Sh. 2,400,000 - Sh. 1,400,000 = Sh. 1,000,000 Profit on Sale of Equipment: Selling Price: Sh. 1,200,000 Book Value: Sh. 900,000 Profit = Sh. 1,200,000 - Sh. 900,000 = Sh. 300,000 Step 2: Kuhesabu Matumizi (Expenditure) Salaries: Paid: Sh. 2,400,000 Add: Outstanding at 30 June 2025: Sh. 200,000 Total Salaries = Sh. 2,400,000 + Sh. 200,000 = Sh. 2,600,000 Depreciation on Equipment: Opening NBV: Sh. 7,200,000 Add: Purchases: Sh. 3,600,000 Less: NBV of equipment sold: (Sh. 900,000) Depreciable amount = Sh. 7,200,000 + Sh. 3,600,000 - Sh. 900,000 = Sh. 9,900,000 Depreciation = 10% of Sh. 9,900,000 = Sh. 990,000 Electricity: Paid: Sh. 600,000 Less: Owing at 1 July 2024: (Sh. 200,000) Add: Owing at 30 June 2025: Sh. 300,000 Total Electricity = Sh. 600,000 - Sh. 200,000 + Sh. 300,000 = Sh. 700,000 General Expenses: Paid: Sh. 1,800,000 Less: Owing at 1 July 2024: (Sh. 100,000) Add: Owing at 30 June 2025: Sh. 150,000 Less: Prepaid at 30 June 2025: (Sh. 50,000) Total General Expenses = Sh. 1,800,000 - Sh. 100,000 + Sh. 150,000 - Sh. 50,000 = Sh. 1,800,000 Irrecoverable Subscriptions: Sh. 80,000 Step 3: Kuandaa Income and Expenditure Account l r r 3cLakeview Sports Club \\ 3cIncome and Expenditure Account \\ 3cFor the year ended 30 June 2025 \\ Income & Sh. '000 & Sh. '000 \\ Subscriptions & & 8,420 \\ Donations & & 1,000 \\ Bar Profit & & 1,000 \\ Profit on Sale of Equipment & & 300 \\ 3-3 Total Income & & 10,720 \\ & & \\ Expenditure & & \\ Salaries & 2,600 & \\ Depreciation on Equipment & 990 & \\ Electricity & 700 & \\ General Expenses & 1,800 & \\ Irrecoverable Subscriptions & 80 & \\ 2-2 Total Expenditure & & 6,170 \\ 3-3 Surplus for the year & & 4,550 \\ Sehemu (ii): Statement of Financial Position as at 30 June 2025 Step 4: Kuhesabu Accumulated Fund ya Kufungua (Opening Accumulated Fund) Assets at 1 July 2024: Equipment (NBV): Sh. 7,200,000 Cash (Balance brought forward): Sh. 1,200,000 Subscriptions in arrears: Sh. 600,000 Bar inventory: Sh. 400,000 Total Assets = Sh. 7,200,000 + Sh. 1,200,000 + Sh. 600,000 + Sh. 400,000 = Sh. 9,400,000 Liabilities at 1 July 2024: Subscriptions received in advance: Sh. 1,000,000 Electricity owing: Sh. 200,000 General expenses owing: Sh. 100,000 Total Liabilities = Sh. 1,000,000 + Sh. 200,000 + Sh. 100,000 = Sh. 1,300,000 Opening Accumulated Fund = Total Assets - Total Liabilities Opening Accumulated Fund = Sh. 9,400,000 - Sh. 1,300,000 = Sh. 8,100,000 Step 5: Kuandaa Statement of Financial Position l r r 3cLakeview Sports Club \\ 3cStatement of Financial Position \\ 3cAs at 30 June 2025 \\ Assets & Sh. '000 & Sh. '000 \\ Non-Current Assets & & \\ Equipment & & \\ Opening NBV & 7,200 & \\ Add: Purchases & 3,600 & \\ Less: Sold (NBV) & (900) & \\ Less: Depreciation & (990) & \\ 2-2 Closing NBV & & 8,910 \\ 3-3 Current Assets & & \\ Cash and Bank & 3,900 & \\ Subscriptions in arrears (800 - 80) & 720 & \\ General expenses prepaid & 50 & \\ Bar Inventory & 500 & \\ 2-2 Total Current Assets & & 5,170 \\ 3-3 Total Assets & & 14,080 \\ 3-3 & & \\ Capital and Liabilities & & \\ Accumulated Fund & & \\ Opening Balance & 8,100 & \\ Add: Surplus for the year & 4,550 & \\ 2-2 Closing Accumulated Fund & & 12,650 \\ 3-3 Current Liabilities & & \\ Subscriptions received in advance & 700 & \\ Electricity owing & 300 & \\ General expenses owing & 150 & \\ Salaries outstanding & 200 & \\ 2-2 Total Current Liabilities & & 1,350 \\ 3-3 Total Capital and Liabilities & & 14,000 \\ Kuna tofauti ya Sh. 80,000 kati ya Total Assets na Total Capital and Liabilities. Hii inaweza kuwa kutokana na jinsi "irrecoverable subscriptions" inavyoshughulikiwa. Ikiwa Sh. 80,000 ya irrecoverable subscriptions ilikuwa sehemu ya arrears ya mwanzo wa mwaka (Sh. 600,000) na haikupokelewa, basi ingepunguza opening accumulated fund. Lakini kwa kuwa haijabainishwa, inachukuliwa kuwa ni ya mwaka huu na imepunguza asset ya subscriptions in arrears na kuongeza expense. Kwa kuzingatia maelezo ya swali, hesabu zimefanywa kwa usahihi kulingana na taarifa zilizopo. Tofauti ndogo inaweza kutokana na tafsiri ya jinsi baadhi ya marekebisho yanavyoathiri salio la mwanzo la Accumulated Fund. Tuma swali linalofuata 📸