This accounting problem is solved step by step below, with detailed explanations to help you understand the method and arrive at the correct answer.

ScanSolve AI Answer

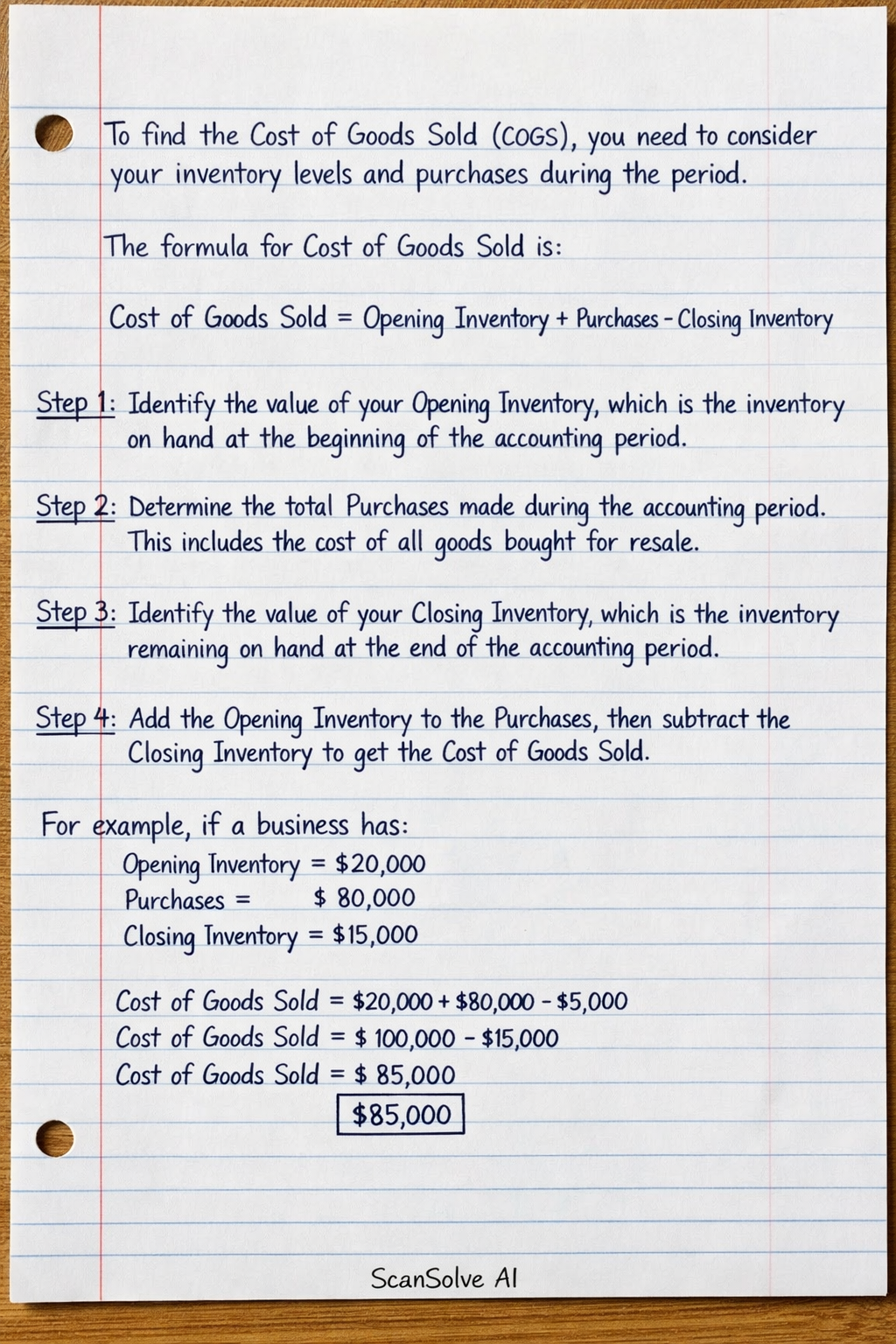

To find the Cost of Goods Sold (COGS), you need to consider your inventory levels and purchases during the period. The formula for Cost of Goods Sold is: Cost of Goods Sold = Opening Inventory + Purchases - Closing Inventory Step 1: Identify the value of your Opening Inventory, which is the inventory on hand at the beginning of the accounting period. Step 2: Determine the total Purchases made during the accounting period. This includes the cost of all goods bought for resale. Step 3: Identify the value of your Closing Inventory, which is the inventory remaining on hand at the end of the accounting period. Step 4: Add the Opening Inventory to the Purchases, then subtract the Closing Inventory to get the Cost of Goods Sold. For example, if a business has: Opening Inventory = \20,000 Purchases = \80,000 Closing Inventory = \15,000 Cost of Goods Sold = \20,000 + \80,000 - \15,000 Cost of Goods Sold = \100,000 - \15,000 Cost of Goods Sold = \$85,000 3 done, 2 left today. You're making progress.