This business/management problem is solved step by step below, with detailed explanations to help you understand the method and arrive at the correct answer.

ScanSolve AI Answer

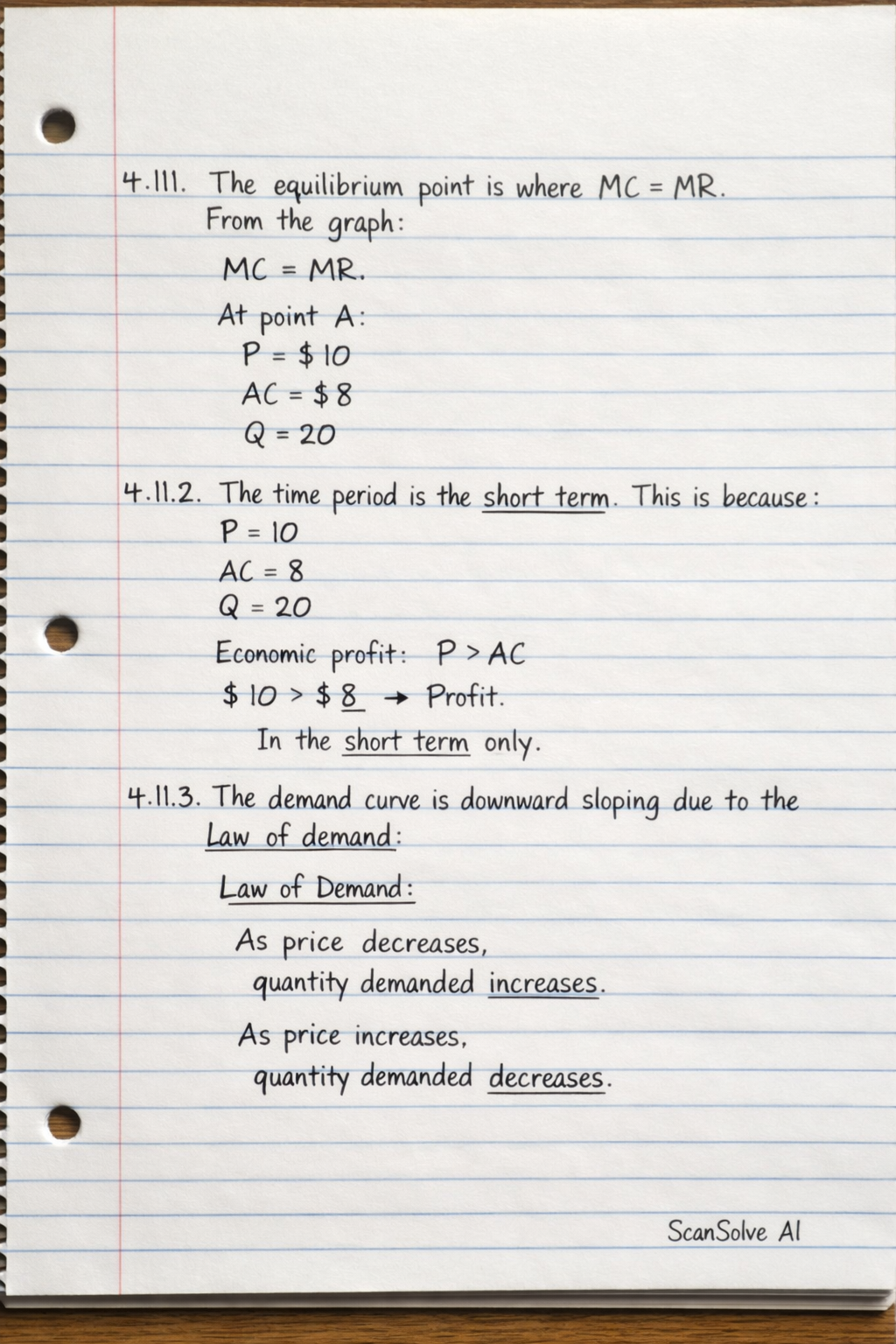

Here are the answers to your questions: 4.11.1. The equilibrium point of an individual firm is where Marginal Cost (MC) equals Marginal Revenue (MR). From the graph, this occurs at point A. 4.11.2. The time period depicted in the graph is the short term. This is because the individual firm is making an economic profit (Price = 10, Average Cost = 8 at equilibrium quantity 20), which is only sustainable in the short run in a perfectly competitive market. 4.11.3. The reason for the downward sloping demand curve of the industry is the law of demand. This law states that, all else being equal, as the price of a good or service decreases, the quantity demanded by consumers will increase, and vice versa. 4.11.4. Businesses in this industry are referred to as price takers because: • There are many small firms producing homogeneous products, meaning no single firm has enough market power to influence the market price. • Firms must accept the market price determined by the overall industry supply and demand. If a firm tries to charge a higher price, consumers will simply buy from competitors. 4.11.5. If new entrants (businesses) affect the perfect market: • The entry of new firms, attracted by economic profits, will increase the overall industry supply. • This increase in supply will cause the industry supply curve to shift to the right, leading to a decrease in the market equilibrium price. • The market price will continue to fall until economic profits are eliminated, and all firms in the industry earn only normal profit in the long run.