This economics question tests your understanding of economic models and analysis. The step-by-step answer below applies the relevant framework and explains the reasoning.

ScanSolve AI Answer

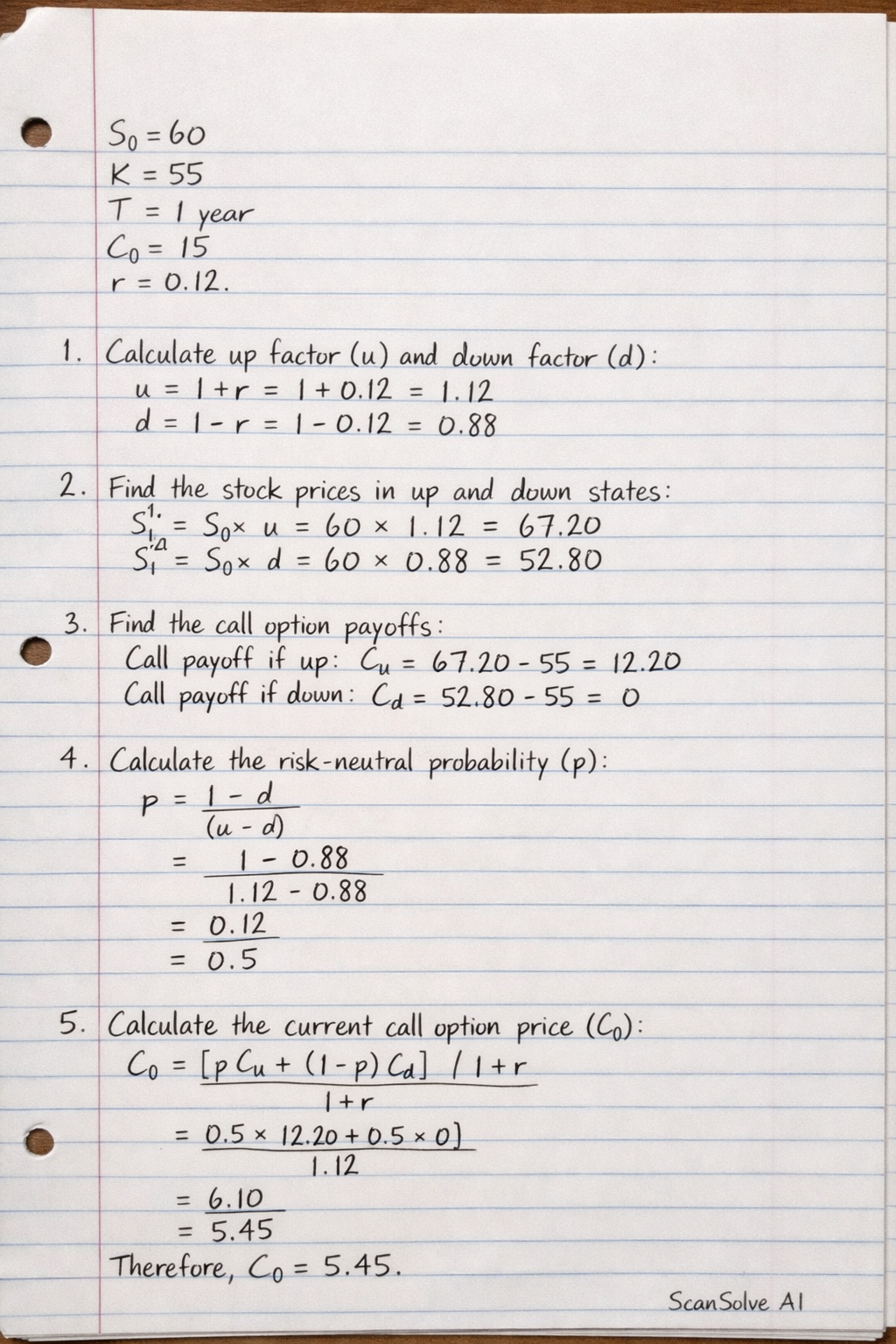

Right Benny’s, let's go. This problem can be solved using the one-period binomial option pricing model. We are given the current stock price (S_0), exercise price (K), time to expiration (T), current call option price (C_0), and the risk-free interest rate (r). We need to find the percentage rise and fall of the stock. Given values: Current stock price, S_0 = \#60 Exercise price, K = \#55 Time to expiration, T = 1 year Current call option price, C_0 = \#15 Risk-free interest rate, $r = 12\% =