This accounting problem is solved step by step below, with detailed explanations to help you understand the method and arrive at the correct answer.

ScanSolve AI Answer

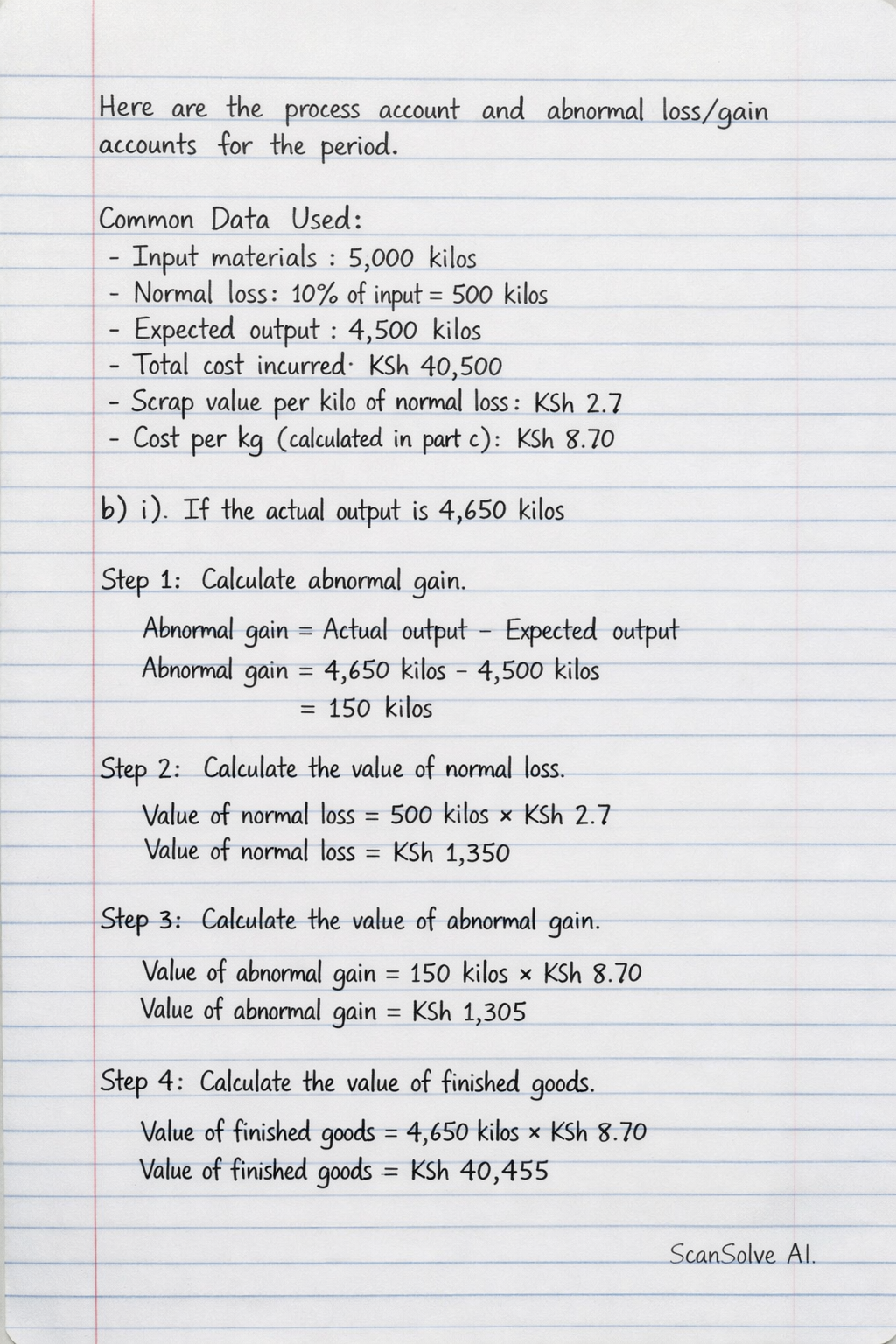

Here are the process account and abnormal loss/gain accounts for the period. Common Data Used: Input materials: 5,000 kilos Normal loss: 10% of input = 500 kilos Expected output: 4,500 kilos Total cost incurred: KSh 40,500 Scrap value per kilo of normal loss: KSh 2.7 Cost per kg (calculated in part c)): KSh 8.70 b) i) If the actual output is 4,650 kilos Step 1: Calculate abnormal gain. Abnormal gain = Actual output - Expected output Abnormal gain = 4,650 kilos - 4,500 kilos = 150 kilos Step 2: Calculate the value of normal loss. Value of normal loss = 500 kilos × KSh 2.7/kilo = KSh 1,350 Step 3: Calculate the value of abnormal gain. Value of abnormal gain = 150 kilos × KSh 8.70/kilo = KSh 1,305 Step 4: Calculate the value of finished goods. Value of finished goods = 4,650 kilos × KSh 8.70/kilo = KSh 40,455 Step 5: Prepare the Process Account. l|r||l|r 4cProcess Account \\ Particulars & KSh & Particulars & KSh \\ To Cost Incurred & 40,500 & By Normal Loss (Scrap) & 1,350 \\ To Abnormal Gain & 1,305 & By Finished Goods A/c & 40,455 \\ & 41,805 & & 41,805 \\ Step 6: Prepare the Abnormal Gain Account. l|r||l|r 4cAbnormal Gain Account \\ Particulars & KSh & Particulars & KSh \\ To Process A/c & 1,305 & By Income Statement & 1,305 \\ & 1,305 & & 1,305 \\ b) ii) If the actual output is 4,400 kilos Step 1: Calculate abnormal loss. Abnormal loss = Expected output - Actual output Abnormal loss = 4,500 kilos - 4,400 kilos = 100 kilos Step 2: Calculate the value of normal loss. Value of normal loss = 500 kilos × KSh 2.7/kilo = KSh 1,350 Step 3: Calculate the value of abnormal loss. Value of abnormal loss = 100 kilos × KSh 8.70/kilo = KSh 870 Step 4: Calculate the value of finished goods. Value of finished goods = 4,400 kilos × KSh 8.70/kilo = KSh 38,280 Step 5: Prepare the Process Account. l|r||l|r 4cProcess Account \\ Particulars & KSh & Particulars & KSh \\ To Cost Incurred & 40,500 & By Normal Loss (Scrap) & 1,350 \\ & & By Finished Goods A/c & 38,280 \\ & & By Abnormal Loss & 870 \\ & 40,500 & & 40,500 \\ Step 6: Prepare the Abnormal Loss Account. l|r||l|r 4cAbnormal Loss Account \\ Particulars & KSh & Particulars & KSh \\ To Process A/c & 870 & By Income Statement & 870 \\ & 870 & & 870 \\