This accounting problem is solved step by step below, with detailed explanations to help you understand the method and arrive at the correct answer.

ScanSolve AI Answer

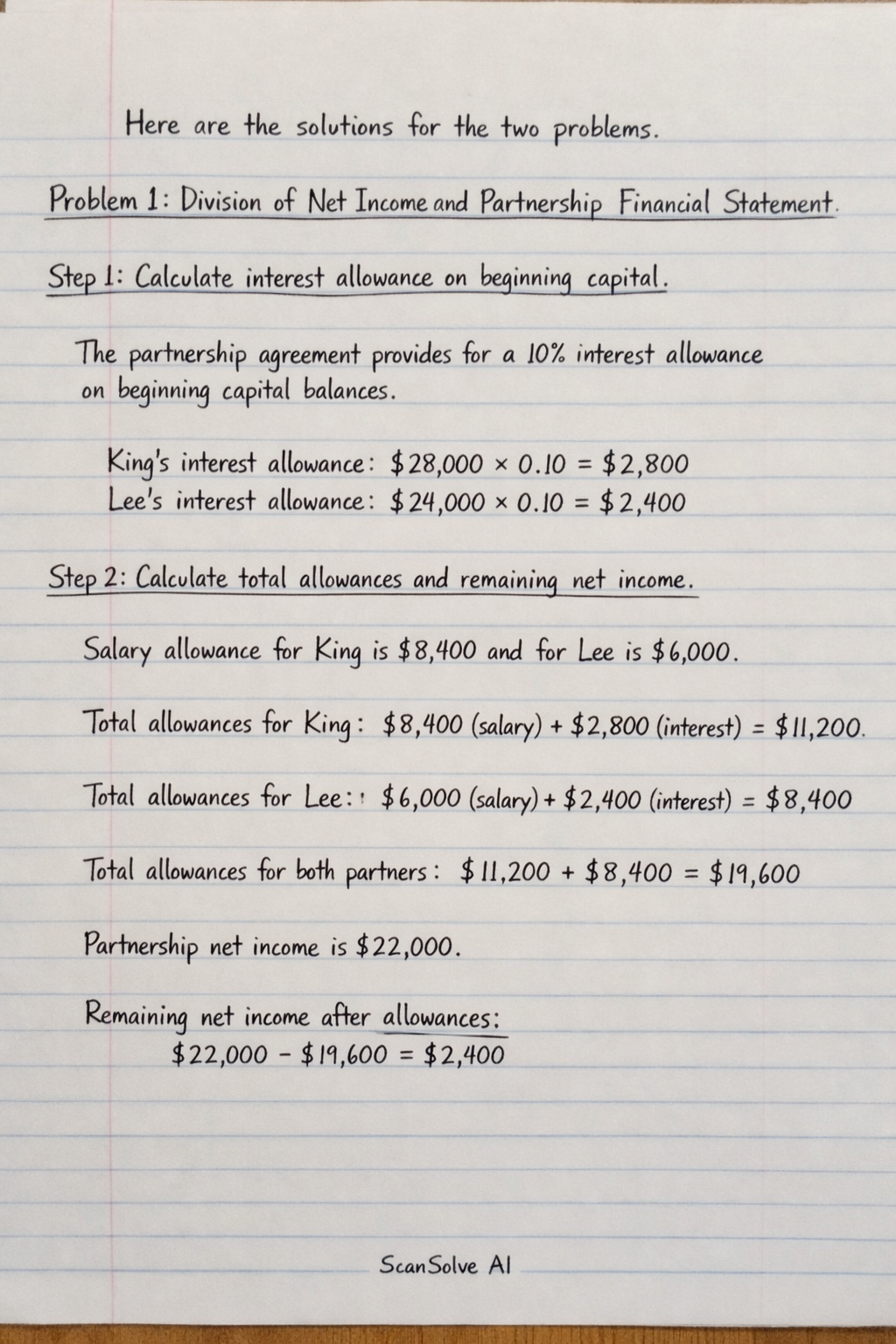

Here are the solutions for the two problems. Problem 1: Division of Net Income and Partnership Financial Statement Step 1: Calculate interest allowance on beginning capital. The partnership agreement provides for a 10% interest allowance on beginning capital balances. King's interest allowance: \28,000 × 0.10 = \2,800 Lee's interest allowance: \24,000 × 0.10 = \2,400 Step 2: Calculate total allowances and remaining net income. Salary allowance for King is 8,400 and for Lee is 6,000. Total allowances for King: \8,400 (salary) + \2,800 (interest) = \11,200 Total allowances for Lee: \6,000 (salary) + \2,400 (interest) = \8,400 Total allowances for both partners: \11,200 + \8,400 = \19,600 Partnership net income is 22,000. Remaining net income after allowances: \22,000 - \19,600 = \2,400 Step 3: Distribute remaining net income and determine total share for each partner. The remaining net income is distributed equally. King's share of remaining net income: (\2,400)/(2) = \1,200 Lee's share of remaining net income: (\2,400)/(2) = \1,200 Total share of net income for King: \11,200 (allowances) + \1,200 (remaining) = \12,400 Total share of net income for Lee: \8,400 (allowances) + \1,200 (remaining) = \9,600 Division of Net Income: | Partner | Salary Allowance | Interest Allowance | Remaining Income | Total Share of Net Income | | :------ | :--------------- | :----------------- | :--------------- | :------------------------ | | King | 8,400 | 2,800 | 1,200 | 12,400 | | Lee | 6,000 | 2,400 | 1,200 | 9,600 | | Total | 14,400 | 5,200 | 2,400 | 22,000 | Step 4: Prepare the Partnership Financial Statement (Statement of Partners' Capital). The statement of partners' capital shows the changes in each partner's capital account over the period. Kingslee Company Statement of Partners' Capital For the Year Ended December 31 | Particulars | King | Lee | Total | | :-------------------- | :---------- | :---------- | :---------- | | Capital, January 1 | 28,000 | 24,000 | 52,000 | | Add: Additional Investment | 2,000 | 2,000 | 4,000 | | Add: Share of Net Income | 12,400 | 9,600 | 22,000 | | Capital, December 31 | 42,400 | 35,600 | 78,000 | --- Problem 2: Partnership Liquidation Journal Entries for Sagastina Initial Balance Sheet Analysis: The problem states total assets are 65,000 and total liabilities and owner's equity are 65,000. However, the sum of listed liabilities (15,000 Notes Payable + 16,000 Accounts Payable = 31,000) and listed capital accounts (15,000 Saga + 17,000 Courage + 1,200 Tina = 33,200) is 31,000 + 33,200 = 64,200. There is an 800 discrepancy (65,000 - 64,200 = 800). To balance the initial balance sheet, this 800 is assumed to be unrecorded capital distributed among partners based on their income ratio (3:2:1). Saga: 800 × (3)/(6) = \400 Courage: 800 × (2)/(6) = \266.67 Tina: 800 × (1)/(6) = \133.33 Adjusted initial capital balances: Saga: 15,000 + 400 = 15,400 Courage: 17,000 + 266.67 = 17,266.67 Tina: 1,200 + 133.33 = 1,333.33 Step 1: Record the sale of noncash assets. Noncash assets include Accounts Receivable (15,000), Equipment (35,000), and Inventory (18,000). Accumulated Depreciation (8,000) reduces the book value of equipment. Book value of noncash assets: \15,000 + \35,000 + \18,000 - \8,000 = \60,000 The assets are sold for 80,000 cash. Gain on realization: \80,000 (sale price) - \60,000 (book value) = \20,000 The journal entry records the cash received, removes the book value of assets, and recognizes the gain. l r Cash & \80,000 \\ Accumulated Depreciation & \8,000 \\ Accounts Receivable & & \15,000 \\ Equipment & & \35,000 \\ Inventory & & \18,000 \\ Gain on Realization & & \20,000 \\ (To record sale of noncash assets) & & \\ Step 2: Distribute the gain on realization to partners' capital accounts. The gain on realization is 20,000. The income ratio is 3:2:1 (total 6 parts). Saga's share of gain: \20,000 × (3)/(6) = \10,000 Courage's share of gain: \20,000 × (2)/(6) = \6,666.67 Tina's share of gain: \20,000 × (1)/(6) = \3,333.33 The journal entry debits Gain on Realization and credits each partner's capital account. l r Gain on Realization & \20,000 \\ Saga, Capital & & \10,000 \\ Courage, Capital & & \6,666.67 \\ Tina, Capital & & \3,333.33 \\ (To distribute gain on realization to partners) & & \\ Step 3: Record the payment of liabilities. Total liabilities: Notes Payable 15,000 + Accounts Payable 16,000 = 31,000. The journal entry debits the liability accounts and credits Cash. l r Notes Payable & \15,000 \\ Accounts Payable & \16,000 \\ Cash & & \31,000 \\ (To record payment of liabilities) & & \\ Step 4: Distribute remaining cash to partners. First, calculate the final capital balance for each partner after distributing the gain and adjusting for the initial discrepancy: Saga, Capital: 15,400 (adjusted initial) + 10,000 (gain) = \25,400 Courage, Capital: 17,266.67 (adjusted initial) + 6,666.67 (gain) = \23,933.34 Tina, Capital: 1,333.33 (adjusted initial) + 3,333.33 (gain) = \4,666.66 Total Capital to be distributed: 25,400 + 23,933.34 + 4,666.66 = \54,000. Next, calculate the final cash balance: Initial Cash: 5,000 Add: Cash from sale of assets: 80,000 Less: Cash paid for liabilities: 31,000 Final Cash balance: 5,000 + 80,000 - 31,000 = \54,000. The final cash balance matches the total capital to be distributed. The journal entry debits each partner's capital account and credits Cash. l r Saga, Capital & \25,400 \\ Courage, Capital & \23,933.34 \\ Tina, Capital & \4,666.66 \\ Cash & & \54,000 \\ (To distribute remaining cash to partners) & & \\ Send me the next one 📸