This mathematics problem involves applying core mathematical principles and formulas. Below you will find a complete step-by-step solution with detailed explanations for each step, helping you understand not just the answer but the method behind it.

ScanSolve AI Answer

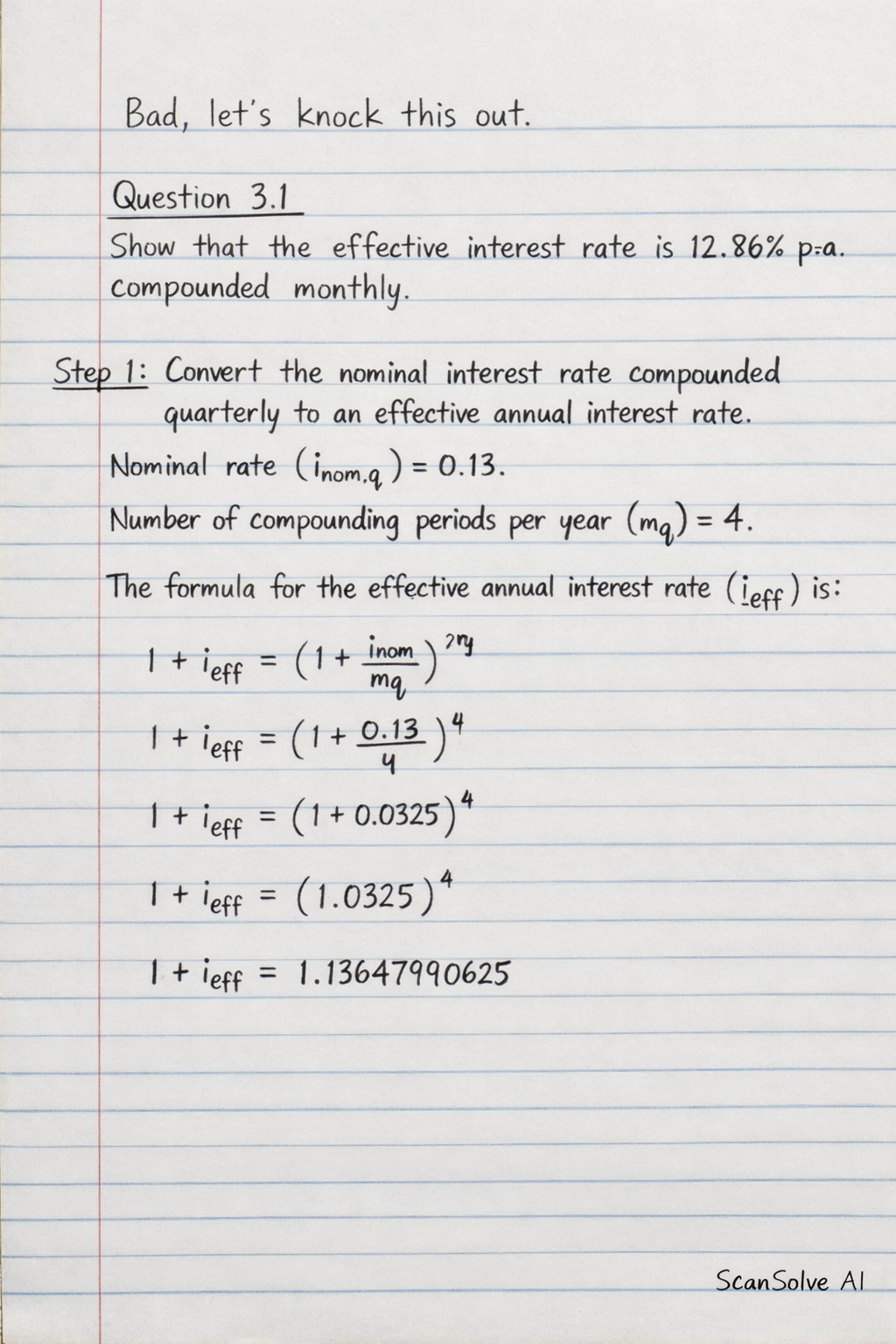

Question 3.1 Show that the effective interest rate is 12.86% p.a. compounded monthly. Step 1: Convert the nominal interest rate compounded quarterly to an effective annual interest rate. The given nominal interest rate is 13% p.a. compounded quarterly. Nominal rate (i_nom,q) = 0.13. Number of compounding periods per year (m_q) = 4. The formula for the effective annual interest rate (i_eff) is: 1 + i_eff = (1 + i_nom,qm_q)^m_q 1 + i_eff = (1 + (0.13)/(4))^4 1 + i_eff = (1 + 0.0325)^4 1 + i_eff = (1.0325)^4 1 + i_eff = 1.13647990625 Step 2: Convert the effective annual interest rate to an equivalent nominal interest rate compounded monthly. Let the nominal interest rate compounded monthly be i_nom,m. Number of compounding periods per year (m_m) = 12. The formula relating effective annual rate to nominal monthly rate is: 1 + i_eff = (1 + i_nom,mm_m)^m_m 1.13647990625 = (1 + i_nom,m12)^12 Take the 12th root of both sides: (1.13647990625)^1/12 = 1 + i_nom,m12 1.010720000 = 1 + i_nom,m12 i_nom,m12 = 1.010720000 - 1 i_nom,m12 = 0.010720000 i_nom,m = 0.010720000 × 12 i_nom,m = 0.12864 Convert to a percentage and round to two decimal places: i_nom,m = 0.12864 × 100\% = 12.864\% ≈ 12.86\% Thus, the effective interest rate is 12.86\% p.a. compounded monthly. Question 3.2 How many full monthly repayments would Jake pay? Step 1: Identify the loan details and the monthly interest rate. Loan amount (P) = R600 000. Monthly payment (X) = R9 000. The nominal interest rate compounded monthly is 12.864\% (from 3.1, using the unrounded value for accuracy). Monthly interest rate (i) = (0.12864)/(12) = 0.01072. Step 2: Use the present value annuity formula to solve for the number of payments (n). The formula is: P = X 1 - (1 + i)^-ni Substitute the known values: 600\,000 = 9\,000 1 - (1 + 0.01072)^-n0.01072 Divide by 9 000 and multiply by 0.01072: (600\,000 × 0.01072)/(9\,000) = 1 - (1.01072)^-n 0.714666667 = 1 - (1.01072)^-n Rearrange to solve for (1.01072)^-n: (1.01072)^-n = 1 - 0.714666667 (1.01072)^-n = 0.285333333 Take the natural logarithm of both sides: -n (1.01072) = (0.285333333) -n (0.01066310) = -1.25441800 n = (-1.25441800)/(-0.01066310) n ≈ 117.639 The number of full monthly repayments Jake would pay is 117. Question 3.3 What will the final payment be? Step 1: Calculate the outstanding balance after 117 full payments. Number of full payments (k) = 117. Loan amount (P) = R600 000. Monthly payment (X) = R9 000. Monthly interest rate (i) = 0.01072. The formula for the outstanding balance (B_k) after k payments is: B_k = P(1+i)^k - X ((1+i)^k - 1)/(i) B_117 = 600\,000(1.01072)^117 - 9\,000 (1.01072)^117 - 10.01072 Calculate (1.01072)^117 ≈ 3.46879800. B_117 = 600\,000(3.46879800) - 9\,000 (3.46879800 - 1)/(0.01072) B_117 = 2\,081\,278.80 - 9\,000 (2.46879800)/(0.01072) B_117 = 2\,081\,278.80 - 9\,000(230.2983208955) B_117 = 2\,081\,278.80 - 2\,072\,684.89 B_117 = R8\,593.91 Step 2: Calculate the final payment, which includes interest on the outstanding balance for the last period. Final payment = B_117(1+i) Final payment = R8\,593.91 × (1 + 0.01072) Final payment = R8\,593.91 × 1.01072 Final payment = R8\,685.99 The value of Jake's final payment is R8 685.99. Question 3.4 What did the car cost Jake in total by the time it is paid off? Step 1: Calculate the total amount paid. Total payments = (Number of full payments × Monthly payment) + Final payment Total payments = (117 × R9\,000) + R8\,685.99 Total payments = R1\,053\,000 + R8\,685.99 Total payments = R1\,061\,685.99 The car cost Jake a total of R1 061 685.99. What's next? 📸